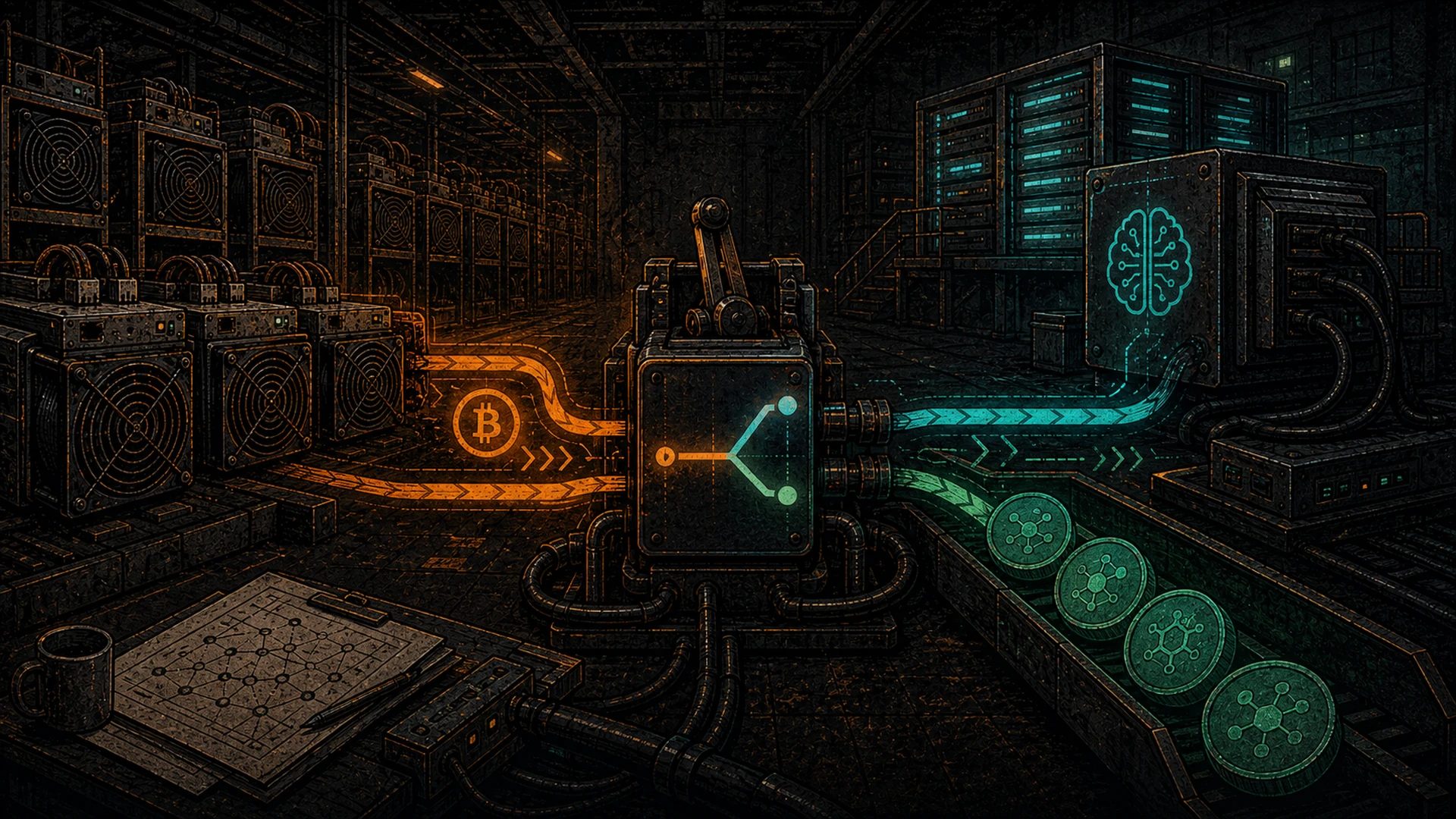

In 2024 and 2025, the largest Bitcoin miners in North America started leaving Bitcoin Hashcenters behind. Not selling rigs — selling compute.

Hut 8 signed a roughly $7B Google-backed AI deal. Core Scientific emerged from bankruptcy reoriented as a CoreWeave GPU colocation host. IREN (Iris Energy) shifted a meaningful slice of capacity toward AI cloud services. TeraWulf announced multi-year AI-compute contracts against its New York sites. Riot, MARA, and Hive each expanded or announced AI-compute lines. CleanSpark, Cipher, and Bitfarms publicly reaffirmed a BTC-core posture — for now.

The industry’s public-company consensus through Q1 2026 is that AI tokens per megawatt are worth more than Bitcoin blocks per megawatt. They’re probably right for those businesses. They are not right for you.

This is not a dunking piece. The pivots are rational for operators answerable to shareholders with quarterly earnings calls. It is an editorial piece about a fork in the road — and about the path that isn’t trending, because that path is still the one the individual pleb gets to walk. The great restructuring of North American Bitcoin infrastructure is a corporate story. The Hashcenter story — the owner-operated, sovereign-workload story — has not ended. It has simply stopped being the fashionable vehicle for institutional capital.

Let’s walk through what actually happened, why it happened, what got traded away in the transaction, and why the individual response to all of it is not despair. It’s the opposite.

What the pivots actually are

A short, factual tour through the public-miner AI pivot, with the caveat that deal specifics move fast and any figure here should be cross-checked against the most recent 10-Q or press release before quoting.

Hut 8. The headline deal of the cycle: a multi-billion-dollar arrangement anchored by Google, converting a major US site toward GPU colocation for AI training and inference workloads. Widely reported at approximately $7B in aggregate commitments over the contract life. Hut 8 retains Bitcoin mining capacity but has publicly telegraphed AI as the forward growth vector.

Core Scientific. Emerged from Chapter 11 in 2024 and pivoted hard into AI colocation, with CoreWeave as the anchor tenant on repurposed sites. The business model shift is explicit: from operating ASICs for the company’s own account to renting power-and-cooling-shaped real estate to a hyperscaler-adjacent GPU cloud.

IREN (Iris Energy). A meaningful percentage of the company’s hydro-powered capacity — the Prince George, BC site and beyond — has been retooled for AI cloud services marketed directly by IREN. IREN’s pitch sits somewhere between “we colocate” and “we operate an AI cloud of our own.”

TeraWulf. Multi-year AI-compute contracts layered on top of the Lake Mariner (NY) campus, leveraging existing grid connections and a nuclear-adjacent power story. Public disclosures in 2025 pointed to an AI unicorn as counterparty.

Riot Platforms. More measured than Hut 8 or Core Scientific. Riot’s AI-compute announcements through early 2026 have been incremental, centered on Texas capacity, and framed as diversification rather than pivot.

MARA Holdings. Still the largest BTC-centric public miner by self-reported hashrate. AI-compute activity exists but is exploratory. The company has publicly argued that Bitcoin-only plays preserve optionality; its critics argue it’s slower to monetize the AI narrative premium. Both can be true.

Hive Digital Technologies. The earliest mover. Rebranded from Hive Blockchain to Hive Digital in 2022 specifically to telegraph a multi-compute future, and by 2026 runs a substantial GPU fleet alongside ASICs. Hive’s retail shareholder base made them comfortable running this narrative earlier than peers.

The holdouts (briefly). CleanSpark, Cipher Mining, and Bitfarms have remained BTC-core through Q1 2026, each for slightly different reasons — CleanSpark’s acquisition-led growth thesis, Cipher’s greenfield expansion pipeline, Bitfarms’ post-consolidation reset. None of them have ruled AI out; they’ve simply not signed the headline deals.

Taken together, roughly half the public North American miner market capitalization now has AI-compute as a stated growth vector. That’s a fast industry consensus by any measure.

Why they did it (the honest business case)

It is worth stating the pivot case clearly, without snark, because if you don’t understand why these companies did this you won’t understand what they gave up.

AI revenue per MW far outpaces Bitcoin revenue per MW at 2024–2026 market conditions. A megawatt hosting H100s or H200s on a multi-year contract at hyperscaler-adjacent pricing produces materially more top-line revenue than a megawatt of ASICs at 2025–2026 hashprice. The exact multiple depends on assumptions, but no public-miner CFO has contested the direction — only the durability.

Big Tech is power-constrained and needs capacity yesterday. OpenAI, Anthropic, Google, Meta, CoreWeave, and Oracle are all fighting for grid interconnects. The public miners already have the interconnects. They have substations, cooling water rights, transmission agreements, land, and in some cases multi-year power purchase agreements. A new-build hyperscaler campus takes five to seven years. A miner-to-AI conversion can take twelve to twenty-four months. That arbitrage is the entire deal flow.

Public-company incentive structure rewards the pivot. Quarterly earnings calls, analyst coverage, stock multiple expansion against “AI infrastructure” comparables (Applied Digital, Iris pre-pivot, CoreWeave post-IPO) — the market awards a higher multiple to contracted-revenue AI compute than to hashprice-exposed Bitcoin mining. Management teams are hired to maximize shareholder return inside a given risk budget. The pivot is the trade that math indicates.

Stranded-asset hedging. The 2024 halving compressed miner economics. An ASIC depreciates on a schedule measured in halvings; a GPU cloud contract amortizes on a schedule measured in CFO conversations. If you believe Bitcoin mining will be increasingly concentrated in low-cost-energy jurisdictions outside North America, it is rational to redeploy North American grid access toward workloads that value proximity to fiber and datacenter expertise more than they value electricity price alone.

None of this is a moral failure. It is, in a capitalist sense, the correct answer for a publicly-traded company whose shareholders expect growth. We give these operators full credit for making an intelligent call about their circumstances. Standing on the shoulders of every mining company that built grid infrastructure in North America — including the ones that are now pivoting — is what made the counter-path we walk possible. Some of the BTC-mining software, site design, firmware work, and operator playbook that D-Central learned from came from these exact companies. That debt is real.

The interesting question is not whether the pivot is rational. It is what, specifically, the pivot trades away — and whether that trade looks different if you aren’t a public company.

What they gave up (the Hashcenter-vs-datacenter frame)

This is the piece most business coverage misses, because business coverage sees compute as compute.

A Hashcenter is owner-operated. The workload — proof-of-work hashing against the Bitcoin network — is chosen by the operator. The hardware is commodity: ASICs, power supplies, control boards, firmware the operator controls. The scale is often small. A Hashcenter can be a single S19 in a shed, a twenty-unit container in a rural lot, or a large site that remains owner-run on owner-chosen software. The defining feature is not size. It is sovereignty over the workload.

A datacenter — in the hyperscaler sense that the public-miner pivot is pointing toward — is multi-tenant, leased, bound by uptime SLAs, subject to customer-driven workload definition, and effectively a power-and-cooling reseller. When Hut 8 hosts Google-routed GPU workloads, Hut 8 does not choose what those GPUs compute. Google does. When Core Scientific hosts CoreWeave capacity, Core Scientific does not know whether that rack is running OpenAI training, a Meta inference fleet, or an Anthropic evaluation harness. CoreWeave does. The operator becomes a landlord. A sophisticated landlord with very specialized real estate, but a landlord.

That is the trade. Not compute-to-compute — sovereignty-to-tenancy. The miner who chose, every block, what pool to point at and what firmware to run, becomes the operator who negotiates a master services agreement, installs the tenant’s software stack, and routes the tenant’s network. The rent is higher than the mining revenue was. The rent next year depends entirely on the tenant’s AI roadmap, the tenant’s procurement strategy, the tenant’s willingness to renew, and the tenant’s own capital position.

This is not a criticism. It is a description. Some pivoting miners understand this clearly and price it into their strategy. Some retail investors don’t, and are pricing these businesses as if they were still sovereign operators with upside exposure to Bitcoin.

The Hashcenter-to-datacenter pivot isn’t leaving compute behind. It is leaving sovereignty over the workload behind. That’s the whole frame.

The centralization consequence

Zoom out a layer. What happens to the global compute landscape when a substantial chunk of power-contracted miner capacity becomes AI compute center capacity?

It consolidates. It consolidates specifically into the handful of buyers who have the capital, the model IP, and the commercial distribution to absorb multi-hundred-megawatt contracts. That buyer list is short: Microsoft / OpenAI, Google, AWS / Anthropic, Meta, CoreWeave, Oracle. Most end-user inference globally already flows through one of those six APIs. As miner capacity flows in, a larger share of humanity’s reasoning-on-demand is routed through a smaller number of commercial gates.

Bitcoin’s security budget is a function of distributed hashrate. Ask a miner about the importance of hashrate decentralization and you’ll get an articulate answer — that is the company’s entire legitimacy story. The same operators, pivoting their capacity toward hyperscaler AI, are by construction consolidating inference capacity. Both of these things can be true at the same time, and both are.

The honest framing: the pivot is good for the pivoting companies and their shareholders, defensible on financial and operational grounds, and — simultaneously — a net reduction in decentralization at the ecosystem level. It increases the share of global cognition that flows through six corporate APIs. That is an observable consequence of the strategy, not a moral attack on the strategy.

The broader version of this argument is the case for self-sovereign LLMs. The point is not that hyperscaler models are bad. The point is that the default routing of human reasoning through a small number of API providers is a civilizational risk profile — independent of whether any individual provider is trustworthy today. The decentralization logic that ties Bitcoiners to self-custody ties directly to the same logic on AI inference.

If you accept that frame, the public-miner pivot is not a neutral corporate reshuffling. It is one vector — a big one — of compute consolidation.

The individual’s counter-move

Here is the part the AI-pivot coverage almost never includes: public-miner strategy does not constrain individual plebs.

Your S19 shed is still your S19 shed. Your used 3090 rig is still yours. The ASIC itself never runs the inference — it’s purpose-built SHA-256 silicon, and you can’t run AI on a Bitcoin miner directly; what carries over is the site, the grid access, and the heat. Your Hashcenter — whatever size — is still sovereign. The pivoting public miners do not own your hardware, do not set your electricity rate, do not define your workload, and do not require your hosting agreement. The counter-path is still fully open. In fact, it is more relevant than it was five years ago, for a specific reason.

As hyperscalers consolidate inference, sovereign AI on owned hardware becomes more important, not less.

This is the sovereign-AI frame stated plainly. If 95% of inference flows through six APIs, the 5% that doesn’t — the models you pull to disk, the weights you quantize yourself, the context you never send to a third-party endpoint, the prompts you refuse to have logged — carries outsized value. It is the only path that preserves the freedoms that Bitcoiners already preserve with self-custody: no counterparty, no permissioning, no content filter someone else chose, no quarterly earnings pressure shaping the tool.

Individual plebs have advantages the hyperscalers don’t want and wouldn’t pursue:

- No compliance overhead. You do not answer to SOC 2, HIPAA, or a government procurement cycle. You can run the open-source model you prefer, at the quantization you prefer, with no legal review.

- No quarterly earnings. Your Hashcenter doesn’t have to report a KPI next Thursday. You can run an obsolete model for three years because it works for you. Hyperscalers cannot.

- Choice of uncensored or censored model. You pick. Llama, Qwen, DeepSeek, Mixtral, Gemma, the newer permissively-licensed experiments — you run what fits your use case and your values.

- Zero margin to a middleman. Electricity and amortized hardware, that’s your cost. No per-token markup, no rate-limit escalator, no surprise pricing change.

- Heat is a feature, not a line item. Hyperscalers must dump their thermal waste. You can heat your workshop or your home with yours. This is a structural advantage that no hyperscaler will ever capture.

None of this replaces Claude or GPT at the frontier. It isn’t meant to. The point is not “run a local 70B and never touch an API again.” The point is that you get to choose what runs locally and what you route outward — and as hyperscaler dependency deepens elsewhere, that choice compounds in value.

For the philosophical anchor of this path, the argument is laid out at length in our Sovereign AI for Bitcoiners: A Manifesto. The practical on-ramp for readers new to the idea is A Pleb’s Guide to Self-Hosted AI.

Where D-Central lands

D-Central’s position on this is unambiguous and boring.

We do not compete with Hut 8. We do not bid for hyperscaler AI contracts. We do not operate a datacenter. We do not seek one. We ship hardware, firmware, and heaters to the individuals who want to run their own Hashcenter — whether that workload is Bitcoin hashing today, local inference tomorrow, or both in the same chassis next year. Everything we build is one more layer decentralized than what existed before.

On the AI side specifically: our contribution is open-source, not a black box. The whole sovereign-inference stack — Ollama, llama.cpp, Open WebUI, the open-weight models — already runs on hardware you own, and our job is to make that pleb-tier path easier, not to sell you a datacenter. Our flagship DCENT_OS (in public beta as of July 2026, GPL-3.0) carries the same instinct from mining firmware into the rest of the stack: own your compute, read the source, trust no one. If you’re weighing where it sits next to the established open options, our mining firmware comparison lays out the feature matrix. This is built for a home, a shop, a small mining shed, a garage, a workshop corner — not for a multi-tenant colo floor — because we believe the counter-path in this article deserves tooling that actually works for it, not abandoned GPUs and duct tape.

That’s the pitch in full. We’re not going to dress it up.

The practical builds that get a reader from “I have an S19” or “I have a 3090” to a working sovereign inference setup are covered in two companion posts: Heating Your Home With Inference and — for the Bitcoin-infrastructure-to-AI conversion path specifically — From S19 to Your First AI Hashcenter. If you’re sourcing hardware, Used RTX 3090 for LLMs in 2026 covers the cheapest credible entry point for running 30–70B-class models at home. And if you want the bottom-rung tutorial before any of that, Install Ollama in 10 Minutes is it.

The common thread across all of them: you own the machine, you choose the workload, you capture the heat, and you pay no margin to a middleman. That is the Hashcenter logic applied to inference. That is the path.

Closing

The great pivot of 2024–2026 is a corporate restructuring story. It is not an individual-sovereignty story. It is a subset of the public-company North American Bitcoin mining industry rationally redeploying its grid access toward a higher-revenue, contracted-tenant workload, because that is what their shareholders pay them to do. They did the math. The math, for them, says go.

The plebs are not going anywhere. The Hashcenter is not dying. It is just no longer the fashionable corporate vehicle. That is a very different thing from being obsolete — the same way self-custody never became fashionable on Wall Street and nevertheless remains correct.

Fashion is not the same as correctness. Public companies optimize for quarterly earnings. The pleb optimizes for owning the outcome — the hardware, the workload, the model weights, the heat. Different utility functions, different destinations.

Hut 8 will run Google’s GPUs well. Core Scientific will keep CoreWeave’s fleet online. IREN and TeraWulf will collect their rent. Good for them. They are not the whole story, and they were never going to be.

Your Hashcenter is still yours.